First-Time Homebuyer Programs California 2026

First-Time Homebuyer Programs in California 2026: What You Qualify For

If you are searching for a home in Temecula Valley or Murrieta and wondering whether you can actually afford it, the answer may surprise you. California has more first-time homebuyer assistance programs in 2026 than most buyers realize — and several of them apply directly to homes in the $679,000–$750,000 range that defines this market. With a 30-year fixed mortgage rate of 6.51% nationally (Freddie Mac, May 21, 2026) and a California average of 6.39% (Bankrate), the right program can meaningfully reduce what you need at the closing table.

Here is exactly what is available, what you qualify for, and what the real numbers look like for Temecula Valley buyers.

CalHFA Dream For All: Up to $150,000 Toward Your Down Payment

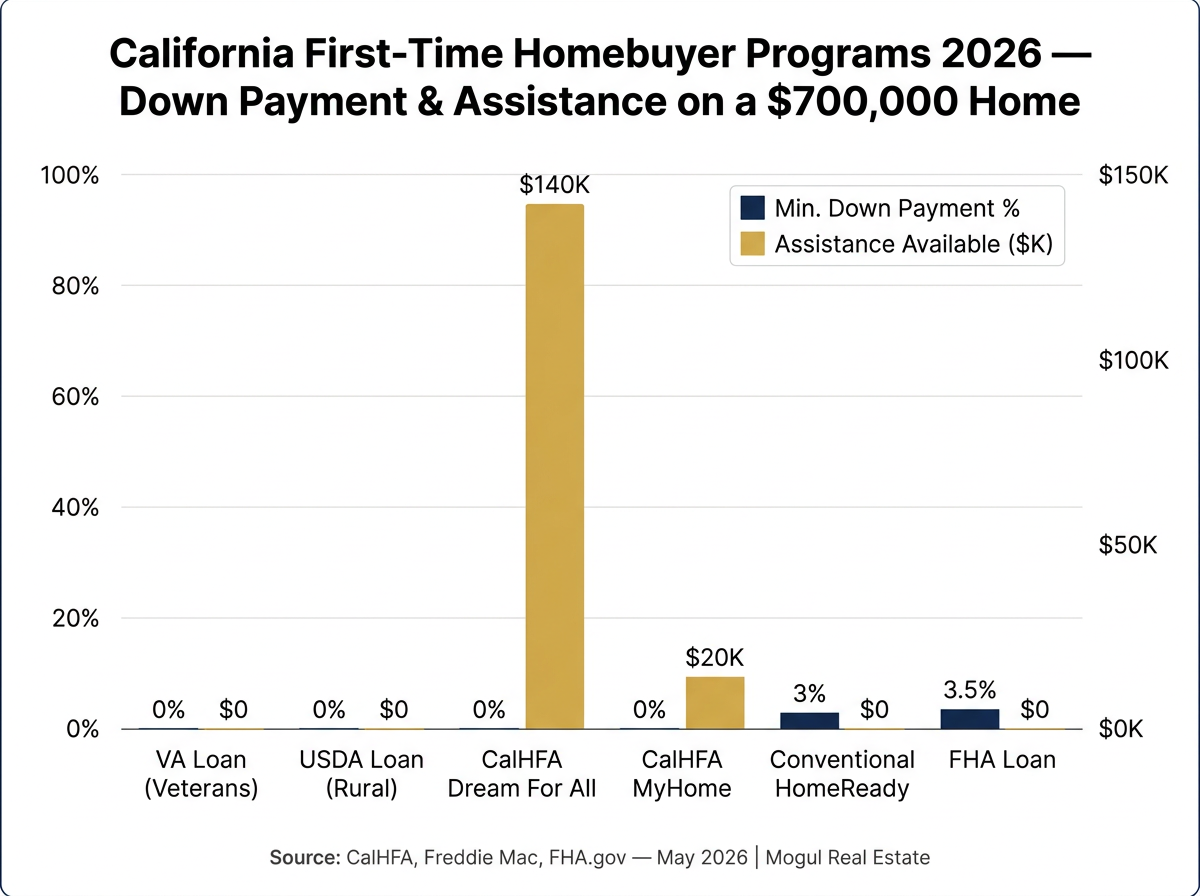

The California Housing Finance Agency (CalHFA) Dream For All program is one of the most powerful tools available to California first-time buyers in 2026. It provides up to 20% of the purchase price or $150,000 in down payment assistance — whichever is less — as a shared appreciation loan.

What "shared appreciation" means for you: CalHFA does not charge monthly payments on this loan. Instead, when you sell or refinance, CalHFA receives the same percentage of the home's appreciated value that it originally contributed. If CalHFA put in 15% of the purchase price, it gets 15% of the gain when you sell.

Real numbers for Temecula Valley: On a $700,000 home (squarely in the local market median), Dream For All could contribute up to $140,000 toward your down payment. That drops your financed loan balance to $560,000 — a meaningful difference in your monthly payment at today's rates.

Who qualifies:

First-time buyer (no ownership interest in a primary residence in the past three years)

California resident

Must meet county income limits — Riverside County's limit is approximately $221,000 for Dream For All, though limits vary. Verify your county's current limit at calhfa.ca.gov before applying.

This program has historically closed quickly when funded. Work with a CalHFA-approved lender and get your pre-approval in place early.

CalHFA MyHome Assistance: A Deferred Junior Loan

CalHFA MyHome pairs with a CalHFA first mortgage to cover your down payment or closing costs through a deferred-payment junior loan — you make no payments on it until you sell, refinance, or pay off the first mortgage.

FHA pairing: Up to 3.5% of the purchase price, with a maximum of approximately $30,205 in standard counties.

Conventional pairing: Up to 3% of the purchase price, with a maximum of approximately $38,633 in higher-cost counties.

Real numbers for Temecula Valley: On a $679,000 home at the lower end of the local range, MyHome on a conventional loan could contribute up to $20,370. That is money you do not have to bring to the closing table.

MyHome can also be layered with the Dream For All program in some scenarios. Speak with a CalHFA-approved lender about combining assistance to maximize your benefit.

FHA Loans: The Low Down Payment Standard

Federal Housing Administration loans remain one of the most accessible paths for first-time buyers statewide. You need a minimum 580 credit score and just 3.5% down — that is $23,765 on a $679,000 home.

FHA loans are available from most lenders across California and carry competitive rates. The trade-off is mortgage insurance: FHA borrowers pay both an upfront MIP (1.75% of the loan amount) and an ongoing annual MIP, which adds to your monthly payment. If you plan to build equity and refinance within a few years, FHA can be a strong entry point.

VA Loans: Zero Down for Veterans and Service Members

If you or your spouse served in the U.S. military, the VA home loan benefit is the most powerful option available. VA loans require zero down payment, carry no private mortgage insurance, and offer competitive rates.

On a $750,000 home at the top of the Temecula Valley market range, a VA loan means you could purchase without writing a single dollar toward a down payment — subject to the VA funding fee, which can be financed into the loan.

Temecula Valley has a significant military and veteran community, given its proximity to Camp Pendleton and March Air Reserve Base. If you qualify, do not leave this benefit on the table. See our full VA home loan guide for eligibility details and how to obtain your Certificate of Eligibility.

USDA Loans: Zero Down in Eligible Rural Areas

The USDA Rural Development loan program offers zero down payment financing for buyers in eligible rural and suburban areas. Some communities adjacent to Temecula Valley may qualify — eligibility is determined by property location, not farm use.

USDA loans also have household income limits. The program is worth investigating if you are considering outlying areas of Southwest Riverside County. Verify property and income eligibility with a USDA-approved lender or at the USDA eligibility map.

Conventional Loans: 3% Down for First-Time Buyers

Through Fannie Mae's HomeReady and Freddie Mac's Home Possible programs, first-time buyers can access conventional financing with as little as 3% down. On a $679,000 home, that is $20,370 — less than FHA requires.

Conventional loans at this down payment level do require private mortgage insurance (PMI), but PMI can be removed once you reach 20% equity — unlike FHA's MIP, which may stay for the life of the loan depending on your down payment amount.

If your credit score is strong (typically 700+), conventional financing often delivers a lower overall cost than FHA over time.

Which Program Is Right for You?

ProgramDown PaymentKey RequirementCalHFA Dream For AllUp to $150,000 assistanceFirst-time buyer, CA income limitsCalHFA MyHomeUp to ~$38,633 (conventional)CalHFA first mortgage requiredFHA3.5% minimum580+ credit scoreVA0%Qualifying military serviceUSDA0%Property in eligible rural areaConventional (HomeReady / Home Possible)3% minimumFirst-time buyer status

FAQ: First-Time Homebuyer Programs in California 2026

Q: Can I combine CalHFA Dream For All with other assistance programs? A: In some cases, yes. CalHFA MyHome can be paired with a CalHFA first mortgage and, depending on the program structure, layered with Dream For All. Work with a CalHFA-approved lender to understand what combinations are currently available and what you specifically qualify for.

Q: What is the income limit for CalHFA Dream For All in Riverside County? A: The Riverside County income limit for Dream For All is approximately $221,000 — but limits are subject to change. Always verify the current figure at calhfa.ca.gov before you apply.

Q: Do first-time homebuyer programs work on Temecula Valley homes in the $700,000 range? A: Yes. Most California programs do not have strict purchase price caps at that level, and CalHFA's Dream For All assistance scales with the purchase price up to $150,000. Programs like FHA and conventional are available at any price point statewide. VA loans also have no purchase price limit (subject to lender requirements).

Q: What credit score do I need to qualify for these programs? A: FHA loans require a minimum 580 score for the 3.5% down option. Conventional programs like HomeReady typically require 620 or higher. CalHFA programs generally require meeting the underlying loan's credit standards. VA and USDA loans have lender-specific minimums that vary.

Q: How do I get started with a first-time homebuyer program in California? A: Start with a pre-approval through a CalHFA-approved lender if you are interested in state assistance programs. For VA loans, obtain your Certificate of Eligibility through the VA first. The Mogul Real Estate team works with buyers throughout this process — contact us and we can connect you with trusted local lenders who specialize in these programs.

Ready to see what you qualify for? Contact us and let's map out your path to ownership.

Browse homes now: Homes for sale in Temecula Valley

Mogul Real Estate — Temecula Valley's local real estate team.